Zero-Based Budgeting, Explained Simply

Zero-based budgeting means assigning every dollar of income to a category before the month begins — until the total left unassigned is zero. It is not about having no money. It is about having no money you cannot account for.

What "zero-based" actually means

The name is confusing to people who hear it for the first time. Zero-based budgeting does not mean your bank account reaches zero. It means your budget equation reaches zero: income minus all assigned categories equals zero.

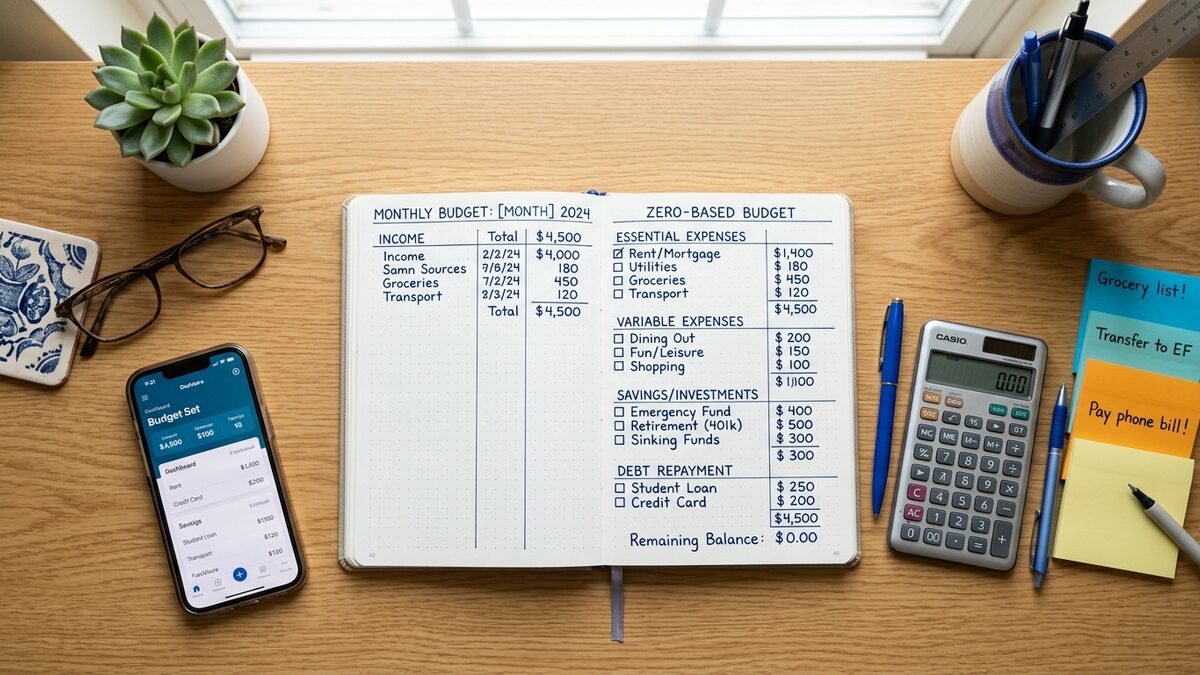

If you make $4,500 this month, you assign that $4,500 to categories — rent, groceries, utilities, savings, investments, fun money, emergency fund contribution — until the full $4,500 is allocated. The point is that every dollar has a destination before the month starts, so there is no untracked pool of money that quietly disappears.

This is different from percentage-based budgets (like 50/30/20) or spending caps, which work backward from the end of the month. Zero-based budgeting is a forward-looking system: you plan before you spend.

The mechanics of building a zero-based budget

The process is the same every month, and it takes about 20–30 minutes the first time. After that it usually takes 10.

- Write down your expected take-home income for the month. Use the actual number, not a round figure. If your income varies, use last month's actual or a conservative estimate.

- List every category of spending you expect this month. Fixed expenses first (rent, loan payments, subscriptions). Variable necessities next (groceries, gas, utilities). Discretionary spending after that (dining, entertainment, clothing). Savings and investment contributions last.

- Assign a dollar amount to each category. Be honest, not aspirational. If you typically spend $400 on groceries, budget $400, not $300.

- Subtract the total from your income. If the result is positive, you have unassigned dollars. Assign them — to savings, debt payoff, or next month's float. If the result is negative, you are over budget before the month starts. Find categories to reduce until the equation balances.

- Track actual spending against each category during the month. The budget is only useful if you know when you are running out in a category.

Why this works better than most budgeting approaches

Most budget failures happen for one of two reasons: the budget is too rigid and gets abandoned after the first unexpected expense, or the budget is too vague ("spend less on food") to actually change behavior.

Zero-based budgeting avoids the second failure mode almost entirely. "Groceries: $420 this month" is concrete. You know when you hit $420. You know if you are at $380 with a week left. The category gives you something to act on.

The flexibility problem is solved by the monthly reset. If you overspent on car repairs in March, you rebuild the budget in April with that in mind. You are not locked into a category amount forever — you are just locked into it for this month, which is a manageable constraint.

The savings trick: Most people treat savings as whatever is left over after spending. In a zero-based budget, savings is a category like rent — it gets assigned at the top, before discretionary spending. This single change is responsible for most of the savings gains people report when switching to this system.

Who zero-based budgeting works best for

It works best for people who want to understand their money rather than just track it. If you have ever reached the end of a month not knowing where $400 went, zero-based budgeting addresses exactly that problem.

It is particularly effective for people in these situations:

- Paying off debt — because every unassigned dollar can be deliberately directed at the debt

- Saving for a specific goal — because you can create a named category and watch it grow

- After an income change — because it forces a reset conversation about priorities

- Couples managing shared finances — because the monthly budget is a shared plan, not just a retrospective report

The honest downsides

Zero-based budgeting takes more active effort than passive approaches. You have to build the budget before the month starts, track against it during the month, and do a brief review at the end. For people who want personal finance to be completely automated, this is not that system.

Variable income makes it harder. The standard workaround is to budget from last month's income — you already know what came in — and hold the current month's income until next month's budget. This creates a one-month buffer and removes the uncertainty. It requires having one month of expenses saved before you start, which takes some runway to build.

A practical first month

Start with eight categories maximum. Combining is fine — "utilities" can be electric, gas, water, and internet in one line. You will discover which categories need to be split after a month of tracking.

Do not make the first budget perfect. Make it honest. A budget based on what you actually spend is more useful than a budget based on what you wish you spent. After one month of honest tracking, you will have the data to make a budget that is both honest and intentional. That is when the system starts producing real results.